Customer Service – Online Transaction & Account Help

Mortgage House provides a secure online Transaction experience that gives you real-time visibility over your loan, balances, redraw, offset, repayments and statements.

This page brings key customer FAQs together in one place so you can get answers quickly and access your loan at any time through the secure Online Transaction Portal.

Online Transaction & App Experience

Do you have an app?

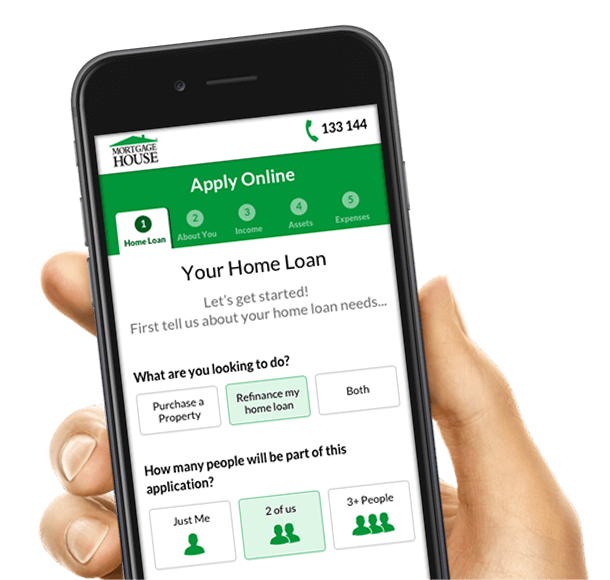

Yes. The secure customer portal works like a modern Transaction app, without the need to download anything.

It is mobile-optimised, fast, and built on the same kind of technology that powers native apps. You simply log in through the Online Transaction Portal, and if you wish, you can save the portal to your phone’s home screen so it appears like a normal app icon.

Account Access & Login

How do I access the online Transaction portal?

You can access your loan and account information at any time using the Online Transaction Portal.

Select Online Transaction, then enter your Username and Password.

What is my username?

Your Username is typically:

- Your Customer ID, or

- The email address you registered when your loan settled.

If you do not recall your Username, you can use the Forgot Username option on the login page.

BSB Numbers & Account Names

What is my BSB number?

Your BSB appears on your Online Login Page once you sign in via the Online Transaction Portal.

If your loan is funded by Mortgage House, the BSB is: Mortgage House BSB: 037-842

You may also find your BSB in:

- Your Welcome Letter

- Your loan documentation

- The Online Transaction Portal

If you have multiple accounts or different funders, your BSB may differ between accounts.

What is my account name?

Your account name is the full legal name you provided at the time you applied for your loan.

For offset accounts, the account name usually appears as:

Firstname Lastname Offset Account

If your legal name has changed, you can request an update through a secure channel after your identity has been verified.

Offset Accounts

Do I have an offset account?

If your loan includes an offset account, it will appear in:

- Your settlement documents, and

- Your Online Transaction dashboard.

What is my offset account number and BSB?

Offset accounts normally share the same BSB as the linked loan account and are usually easy to identify. Offset account numbers often begin with the digit 4.

To confirm your exact offset details:

- Log in to the Online Transaction Portal.

- Select Accounts.

- Choose your Offset account to view the full BSB and account number.

What account is my offset linked to?

Your offset is linked to a specific home loan or loan split so that every dollar in the offset reduces the daily interest charged on that linked loan.

If the offset was included at settlement, you will have received a confirmation with the linked loan details. If it was added later, you will receive a similar confirmation. You can always see the linked loan split in the Online Transaction Portal under Accounts.

Can I order a debit card for my offset account?

If your product includes card access, you can order a Visa debit card directly in the secure portal.

For security and compliance reasons, the card must be ordered by the account holder.

Redraw, Reserved Instalments & Real-Time Access

What is my redraw limit?

Your redraw limit is the amount you have paid ahead of the minimum required repayments. These surplus funds:

- Help reduce daily interest

- Provide a financial buffer

- Become available to withdraw once cleared

To view your redraw limit:

- Log in to the Online Transaction Portal.

- Select Profile Settings.

- Open the Account tab.

- Select Payment Limits.

Redraw limits are calculated automatically based on your repayment history and cannot be manually set or increased. To grow your redraw, you simply pay more than your scheduled repayment.

What is a reserved instalment?

A reserved instalment is one full monthly repayment retained in advance on your loan. It works as a built-in buffer that:

- Reduces the chance of accidental arrears

- Helps cover timing issues from weekends or public holidays

- Continues to lower daily interest because the funds sit against the loan balance

It is not a fee or penalty, and it operates purely to provide protection and smoother repayment behaviour.

Do I have real-time redraw?

If you have a premium product with an active annual facility fee, you may have access to unlimited real-time redraw, subject to cleared funds.

You can check your redraw facility, balance, and transaction history at any time through the Online Transaction Portal.

Interest Calculations & Repayment Behaviour

How are interest-only repayments calculated?

Interest on your home loan is calculated daily on your outstanding balance:

Daily Interest = (Annual Interest Rate ÷ 365) × Daily Loan Balance

The daily interest amounts are added together, and the total becomes your interest charge for that month.

Because:

- Different months have different numbers of days, and

- Your balance may change with redraws and extra repayments,

your interest-only repayment can change slightly from month to month.

Why are interest-only repayments monthly?

Interest-only repayments must be monthly because the exact interest amount is not known until daily interest has been calculated for the full month.

For accuracy and to avoid under- or over-charging, interest-only loans cannot be set as fixed weekly or fortnightly repayments.

Next Repayment Date & Amount

When is my next repayment due?

You can view your next scheduled repayment date and amount in the Online Transaction Portal:

- Log in to the portal.

- Select Repayments.

- Your next repayment date and amount will be displayed.

Generally:

- The repayment date is the same day of each month as your original settlement date.

- If your loan settled on the 30th or 31st, the repayment may fall on the last valid day of shorter months.

Changing Repayment Dates

Can my repayment date be changed?

Monthly repayment dates and interest-charge dates are set in your loan contract and cannot be changed.

You can review your existing schedule at any time via the Online Transaction Portal.

Monthly direct debits – limited flexibility

If you pay by monthly direct debit, a limited timing adjustment may be available:

- The debit can be delayed up to 5 days after the interest-charge date, provided the loan remains fully up to date.

- A delay beyond 5 days may result in arrears under the loan contract.

This flexibility is designed only to assist with short-term timing issues and does not change the contractual repayment date.

Weekly or fortnightly repayments (Principal & Interest only)

Weekly and fortnightly repayment schedules are available only for Principal & Interest loans. To keep the loan compliant:

- Weekly: there must be 4 repayments between each monthly interest-charge date.

- Fortnightly: there must be 2 repayments between each monthly interest-charge date.

If a proposed change results in fewer repayments than required, the loan may fall into arrears and fees may apply.

Why repayment dates cannot move

These rules exist to ensure:

- Accurate daily-interest calculation

- Precise allocation of principal and interest

- Correct conduct reporting on the loan

- Protection against accidental arrears

The monthly repayment and interest-charge dates act as anchors for these calculations, which is why they cannot be moved.

Statements & Documents

How do I get my statements?

All loan statements are available at any time in the secure Online Transaction Portal. Once logged in, navigate to the Statements section to view, download, or print available documents. Online access is free of charge and is usually the fastest way to obtain statements.

Rate Reviews & Loan Variations

Can I get a rate review?

A rate review may be considered when:

- Your loan has been active for more than 6 months.

- Your account has been clear of arrears or dishonours for at least 2 months.

- For construction loans, construction is complete and the final drawdown and Certificate of Occupancy are in place.

- For fixed loans, within the 30 days prior to fixed-rate expiry.

A rate review is often simpler and faster than applying for a new loan because your history and conduct are already known.

Can I convert my loan to interest-only?

In some cases, you may request to convert your repayments to interest-only. This is treated as a loan variation and is subject to:

- Updated customer information

- Current income documents

- A brief serviceability assessment

- Eligibility for the requested interest-only term

Interest-only requests are always subject to credit assessment to ensure the loan remains suitable and serviceable.

Changing Loan Purpose – Investment to Owner-Occupied

How do I change my loan from an investment property to owner-occupied?

If you have moved into a property previously financed as an investment, the loan purpose should be updated to reflect owner-occupation.

You will normally be asked to confirm:

- Your updated residential address via identification

- An updated residential address shown in your ATO records

- Completed internal forms to refresh personal and financial information

Once the information is received and assessed, the loan can be updated so that it correctly reflects owner-occupied status.

E-BSB, Direct Debits, Direct Credits, PEXA, BPAY

What does the “E” in my BSB mean?

The “E” stands for electronic. Accounts with an E-prefixed BSB are designed for Direct credits

Cheques and over-the-counter deposits cannot be processed to these accounts, which keeps transactions fast, secure and fully digital.

When are direct debits processed?

Direct debits are processed on business days.

If the scheduled date falls on a weekend or public holiday, the debit is processed on the next business day. This keeps repayments aligned with your contract.

When do direct credits appear?

Direct credits first arrive into a clearing account and are then allocated to individual loans on the next business day, usually late morning. This ensures funds are reconciled accurately to the correct loan.

Can I send loan payments through PEXA?

No. Mortgage House loan accounts are not set up to receive payments through PEXA.

Loan payments should be made via:

- Direct debit

- Direct credit

- BPAY

When are BPAY payments processed?

Outgoing BPAY payments are processed at scheduled times on business days so that funds are forwarded promptly to the biller.

You can review balances, repayments, redraw, offset and transaction history at any time via the Online Transaction Portal.

Review Your Loan Anytime

For repayments, balances, redraw, offset, statements and key account information, log in securely via the Online Transaction Portal.